#FridaysFacts with a #WeekendCall2Action!! – Great guideline tip reminder for all in the industry, LO’s and RE Agents, regarding someone whom is #SelfEmployed! And a #JUICY Call 2 Action for you this weekend! It’s all about taking your pipeline to the #NextLevel! ↓

When it comes to planning some way to make a difference in your own business pipeline, it starts with educating yourself and creating a strategy to implement! The #WeekendCalltoAction is up to you to click here –> NEXT LEVEL LIVE IN DALLAS! And if you didn’t know, there’s already 100+ LO’s signed up, this event is BIG! Like HUGE, and if you want to impact your market place, there’s a discount for the event tickets for the next two days for those that #TakeAction.

#Two4Tuesday – Guideline Day – FNMA Updates galore! Fannie Mae has been busy this month, with several key updates. Some that may just affect your loans in process! So excited for the new 1003 to come out, just as the past the disclosure “roll out” as optional has been post-poned! The actual roll out date will be too, but we just have to wait for the next update that let’s us know when we can roll out the optional use of the new application.

Some good updates this month, and I hear and see other LO’s mentioning that DU seems a little tighter already. This is the second time in the last 90 days that DU has been updated. And this time Fannie is really vague on what was updated, other than specifically identifying “other risk factors”. This comes down to DTI, reserves and LTV, mark my word, some LO is gathering conditions from a loan and in the last 5 days their file has not been re-ran through DU. And when it does on the final time, there will need to be a restructure to make it work. Risk thresholds are being updated and over time after running so many DU run’s we’ll be able to report back to you and let you know what changed. Just remember the basics on DTI for FHA/VA and Conv.

Basics;

FHA – Three buckets depending on how many compensating factors your file has 31/43 & 37/47 & 40/50

VA – One major backend threshold that is mentioned and that is 41. There is also note of use of residual income as a compensating factor. (this has been the loosest one of them all over the years and more recently have had personally a VA loan with as high as 82 DTI close)

Conventional – While it is widely known that conventional goes to 50 DTI (49.999) in the books (ed) and in programming the thresholds of 28/36 are used. So if your file is over that, you should have compensating factors.

Risk is risk and when it comes down to it, there seems no two files are the same. Just watch your risk thresholds on active loans as DU is updated, and keep rocking.

#ThrivingThursday – Happy Birthday Regulation X! June 20th 1975, was the birthday of what is known as Reg X! Or RESPA as it’s commonly known. The Real Estate Settlement Procedures Act. What has Reg X done for you in the mortgage industry? Well this year alone Reg X paid me over 2k, I’ll tell you how. Since I’ve moved to WV 3 years ago, I had my house as a primary residence and per tax law was supposed to be “Homestead” but apparently it was not. Around Feb, sometime a tax assessor showed up in my driveway. I kid you not, I even told him who I was and asked him to make sure he made my taxes go down. We laughed and he verified this was my primary residence. Well not too far into the March I got an escrow “refund” check where my “lender” that was servicing my loan had wayyyyyy too much in an impound account for taxes. So per Reg X, all lenders have to do a balance reconciliation and return to owners any amount over 50 dollars above what is needed. So not only did my taxes go down and my payment drop almost 200 dollars, but I got back like 2k. No joke. This just happened. Almost 4 years after my purchase. Thanks REG X!

So what else does Regulation X do? I detail the four main points today for everyone of my fans to know! #CheckItOut ↓

As you can see Regulation X is still going strong after 44 years! Great law that our government got right over 40+ years ago. And still plays a major part of our #MortgageWorld. It prevents a seller from requiring a certain title company to be used, and why title is typically a closing cost you can shop for. It requires specific amounts for impound (known as escrow accounts) of taxes and insurance. And limits what a lender can take in advance, which is up to 2 months cushion. It prohibits kick backs, fee splitting and referral fees for anything of value, which still to this day is walked as a thin line by many. (Big Violation and is costly for those that do = 10k per violation) Reg X also requires a 15 day notice to consumers if their mortgage is ever transferred and gives consumers a grace period of 60 days if they sent the payment to the “wrong lender” collecting their payments.

These are consumer protection laws and rightfully so, it’s a great day to celebrate Reg X! So if you have questions about this law, reach out to me. You shouldn’t be “marked” late on your mortgage if your servicing is transferred inside the first 60 days. (Grace period I just explained) Happy 44th Reg X, thanks for protecting consumers as you do! 🙂

#WhackedOutWednesday – Get your “Free Report” annually! If you’re looking to purchase “anything” in the near future it’s a good idea to take advantage of the FACT Act (FACTA = Fair and Accurate Credit Transactions Act)! The only place authorized under the FTC and credit reporting agencies (Experian/Equifax/TransUnion) to provide YOU a FREE CREDIT REPORT ANNUALLY is what I’m talking about!

You see what’s whacked out, is people right before they buy something “big” like a car, house, boat etc, should know where you stand. Most do not know. Today I’ll give you all the credit “tips” the pro’s sometimes have you pay for. What you need to know, and need to do with credit is all here. Most people just don’t know what they don’t know, or pay off their credit bills each month thinking that’s a good idea. (It’s not) Credit is imperative for insurance, for buying things, for jobs sometimes, for financial fitness. Your key points are below! ↓

Open new accounts every several years. It’s actually a weight on your credit score, if you just have credit cards for 10 years and no new credit added, that actually hurts you. Maintain and show the bureau’s you can “manage debt” as this is what gives you credit anyhow. So that means DO NOT pay your credit card off every month. What you want to do is maintain these two ratios; Either revolve less than 30% of the balance at all times (which gives you a better score) or revolve less than 50% of the available balance at all times. For example, if you have an available balance of 1k, do not revolve more than 500 dollars, the minute you go over that 50% mark, the bureau’s actually mark your score down.

Another factor is “type” of credit and payment history. Now it’s kind of a given that you should actually “pay” your debts every month, but this seems to be news to some people. lol. Second is type, when it comes to the type of credit, it’s good to have a mortgage, a secured note (like a car), and then 3 or more revolving lines of credit. (all with balances less than the ratios noted above) In all my experience in the mortgage industry (15 years +) I would say of the thousands of credit reports I’ve seen, the best scores (750+ FICO) and credit always seem to have at least 5 trade lines. (as mentioned) So if you think paying “cash for everything” is a good idea your totally wrong.

Credit is actually what #MakesTheWorldGoRound so it’s important that you do somethings to maintain and show you can manage debt. Debt is not necessarily bad, however, there is such a thing as bad debt and good debt. (but that’s another blog for another day) If you want your FREE REPORT — CLICK HERE!

#ThursdaysThoughts – Lender for life mentality and MI Cancellation. Did you know Fannie Mae just did an update on the 15th of this month (May, 2019) that authorizes any servicer to “Solicit” your client for MI Cancellation based on on original value!?

As a reminder there is two ways a conventional loans PMI (Private Mortgage Insurance) can be eliminated. One is borrower requested cancellation of MI, and the other is lender initiated cancellation of MI. Typically, lender initiated cancellation of MI occurs when the amortization schedule reaches 78% LTV. (however I think guides have been updated on this and might be 80% now) This is all based on original value of the home weather 3 years ago, or 7 years ago based on the original amortization schedule of their loan. The other way is borrower initiated cancellation of MI. Which can be based on original value as well as new appraised value.

It’s an eye opener that Fannie Mae is basically giving “permission” for servicers retail departments to solicit your borrower. Fact is they have. It’s in the announcement on the 15th. So as an LO, it’s your job to view the transactions to be a “LENDER FOR LIFE” and have that mentality to help your clients many times not just one. The average consumer does 7-10 mortgages in their life time. Not to mention kids buying homes. So it’s your responsibility to be that person to follow up, don’t just send them a thank you card and or follow up for a year afterwards. It has to be something you do “forever” to help that client.

Today I provide two solutions to do just that, one a service you can input your past clients in to monitor when ever they are looking for a mortgage. You get a trigger lead, and there’s multiple levels of follow marketing that can go with this. It’s “Retain Your Client” also known as Stikkum. CLICK HERE for the trigger lead follow up!

The second solution is a CRM that has follow up campaigns developed for you, and is phenomenal in helping you vet leads to find those action takers. This can and is a must in the mortgage world to have a customer relationship management software that helps you stay in front of your past clients, current clients, and prospects. It’s your responsibility to take that #Lender4Life mentality to help your own clients. CLICK HERE for the LO’s CRM!

The last thing you want is some servicer calling your client to “solicit” them into another loan without you.

#WeekendCall2Action – New 1003 Wrap up!! This weeks been great in breaking down the NEW 1003! My advice is absolutely to embrace this as soon as it comes out! My ending thoughts is this will help LO’s ensure they are asking the right questions during the 1003 stage of a loan!

I absolutely love ♥ this new 1003, and think for those that fill it in completely will gain better results in DU and LP as a result. I love love ♥ the fact it asks if the borrower is a Veteran, and see how the charted flow will help not only interpretation of the risk profile, but show options to assets & income that sometimes LO’s may not be asking. Overall, this is 100% a healthy change for our industry. My suggestion, get to know it now, and you can see it HERE. #KnowYourCraft

I’m in the office taking “I gotta guy” questions and turning scenarios into loans. Why not yours?? #GetOnPoint with #BluePointMtg – CLICK HERE!

#ThursdaysThoughts – New 1003 Week! Today we wrap up the 1003 breakdown we’ve been doing all week and tomorrow I will do a compare contrast and point out the highlights I believe everyone should pay attention too. This has been great breaking it down each day to help LO’s understand the new 1003.

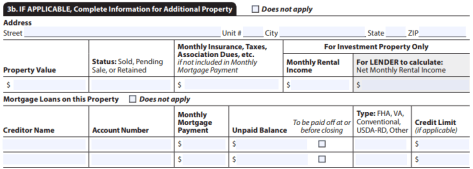

Section 5 is the declaration question section, and is basically all brand new. The current 1003 has 10 questions, the new one has 16! Comparing the two, there’s 3 question on the current dec section that are not even asked, because they are asked elsewhere on the 1003, and then the new 1003 has 9 new questions a LO must ask. This section is broken down into two, 5a, and 5b. About this property and your money for this loan, and about your finances.

And Section 5b ↓

Section 6 is all about the legal acknowledgements and agreements with doing a home loan. It breaks down 6 areas of legal verbiage for the client to sign off on. AND there is two signature lines on the primary borrower’s 1003! (Tomorrow I go over this)

Next up on the 1003 is the very familiar Demographic information page section 7. This is identical to what we have now on the current 1003, I see no evident changes.

The last section of the 1003 is section 8. The Loan Origination information section. And this contains all the same information as on the current 1003 just the the order of which it is portrayed has changed. The company is now first, versus the LO information.

And of course on the last page of the 1003, the borrower’s name goes on the bottom left that coincides with the 1003 of that borrower. I like the flow overall, and there are some new sections, new questions and better information gathered as a whole on this new 1003. I think it takes a lot of the “holes” on the existing 1003 and makes it stand out as questions on the new one. KNOW YOUR CRAFT inside and out. This is a major change and I believe most LO’s are just now starting to take a look at this new one.

Now it’s time to get more loans! #GetOnPoint with #BluePointMtg!

#WednesdaysWisdom – It’s the New 1003 Week – Section 3 & 4 are broken down today! I have to say I really like the “chart” format to every section of the 1003 as I see it. It will require LO’s to ask more questions, and common things missed are listed as questions. I like it a lot. Today we start with section 3 and is the REO section. The instructions at the top of page 4 are just as the other sections, very easy to read and spell out what’s needed.

Section 3 starts off with the REO section of the home being refinanced first. (and is in bold) Otherwish if you do not own any Real Estate, check the box!

Section 3b is a continuation of the REO section for other properties, and so is 3C. Very simple page 5 of the new 1003, and is to detail REO’s owned.

And of course at the bottom of page 4 you have the borrower’s name the information is associated too! Now page 5 Section 4, the loan and property information. Again I like how it starts off and is self explanatory for instructions. The newest thing on here is a FOURTH option for occupancy. And then the 2 questions at the bottom of the first chart.

Then section 4b breaks down other loans on the property they are buying or refinancing. This includes seconds, hard money, or seller carry backs.

Section 4c breaks down rental income and would be filled in on any home that is a 2 unit or more. Primary or investment to indicate the expected monthly rental income. No you do not take 75% in this section, that the underwriter would do in their section for this, just list the full rent expected to be received.

The final section on page 5 is the break down on gifts for the transaction. I like the new 1003 in that it highlights the often missed items on the current 1003 now. This also is put together in a chart like format and gives examples, it’s like selling for LO’s. What a great reminder too.

And guess what’s at the bottom of page 5? You bet the borrower’s name at the bottom left that the information is applied too. I love this new 1003 and the more I analyze it the more I see how it brings to life the issues we have in loans and makes it more transparent for underwriting.

Ok, as I stated in today’s video, I’m in the office taking “I gotta guy” questions to help you bring a 1003 to life!

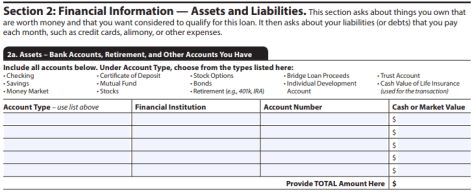

#Two4Tuesday – New 1003 Week – Today we break down section 2 of the new 1003! The flow of the URLA (Universal Residential Loan Application) has definitely changed. But for the better, the instructions are more clear at the top of each page, and information flows nicely in each “charted” section for the borrower. One thing that sticks out to me the most, is the “lists” of items and examples at the top of each charted section, is a great minder to all sales people what types of assets, liabilities, etc there may be.

Section 2 starts off with a nice instructional sentence at the top and moves right into assets first to list the total of value for that section. Again note the lists that this chart shows. Great sales tool in my opinion.

The section 2b is new, and is a great itemization to some of the most commonly missed items on the old 1003. It points out “Other Assets” you have such as an EMD already in escrow, or sweat equity or rent credits or proceeds from a sale of a home. See again the list above the chart. Great section to be on the 1003 and good new edition.

Section 2c is the start for Liabilities and again I like the “chart look”. What’s interesting is that Real Estate is excluded in this section specifically and you are to list all items as debts except mortgages in this section. I wonder how the LOS systems out there will transfer over the debts into this form.

Page 3 is all Section 2, and ends with the “other liabilities” that are often missed to disclose, such as Alimony or Child Support, separate maintenance etc. What sticks out to me again is the name at the bottom of the page 3 that identifies who is the borrower on this application. Their name is to be there so the underwriters know which 1003 belongs to who.

As indicated yesterday there are a few extra forms on the application now. In fact a second borrower has a complete separate application identified just for them. You can see the identification of “Additional Borrower” on the 1003 for any co-borrower on a loan now at the bottom of all pages. (where their name goes too) Another is the unmarried addendum that is needed if they selected unmarried and then a part of the 1003 that is actually filled out by the lender!

And the additional addendum for those that select unmarried in section 1. ↓

I like the flow so far, but what it means in reality is the LO has to have more “apps” taken. Meaning there is more forms to fill out a home loan application. And more specific questions that need to asked and are pointed out inside the application in various sections. Even a portion filled out by the lender. Quite unique. I would have these printed for the first several and go through them the long hand way to learn the new changes. But that’s just me.

As I always indicate, being a master of your own craft starts with the heart of the transaction, which is what underwriters verify information off of, the 1003. All LO’s need to know this like the back of their hand.

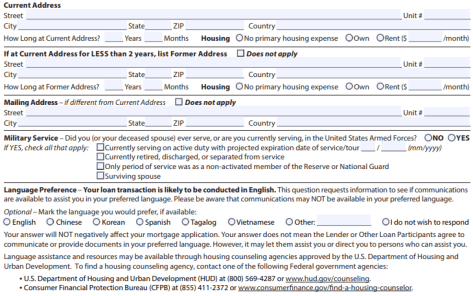

#MondaysMotivation – NEW 1003 Week!! – We are less than two months away from July 2019 when the new 1003 becomes optional. ARE YOU READY? Have you looked at it, and do you understand the new stuff on it, or the things that stick out that changed? Actually section 1 is completely new! And this week we will go through each section and highlight the changes, what’s new, and how it applies to your new process of taking an application.

Today I will break down section 1, and provide my synopsis and point out differences and note-able changes. The biggest change is mulitple people are NOT on 1 application even if married. Only 1 person is. Every person fills out an application and then on the application there is a place to list other borrowers applying for this loan. (however they need to fill out a separate 1003) Again the 1003 claims only 1 social security number and date of birth for “the borrower” on it. And lists the names and total number of borrowers for the loan.

The same flow as the current 1003, just a different look and feel. The second major area on page 1, section 1a is the current address section. Much like the current 1003, the rule of having 2 YEARS HISTORY for EVERYTHING is pointed out. (most commonly missed thing for 1003’s) I love the military declaration section, and it’s interesting they added the new section for the primary language preference. Biggest notable is the radio button options for No Primary Housing Expense, and or Rent or Own. And to the right is an area to identify how much. Check it out ↓

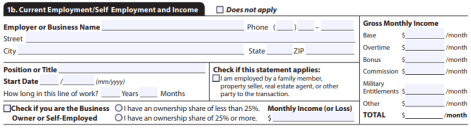

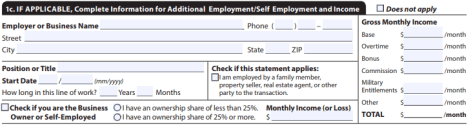

Page 2 starts off with income section, and is considered section 1b. The main thing I like is the fact there is a flow for listing the job and then the amount at that job on the same place on 1003. Must like the current address and amount of that housing expense, this lists the job/self employment and that amount they make. If self employed that box is at the bottom left instead of top right, and has a declaration section for ownership that is new. Then a separate place to indicate income from self employment income. Over the right “gross monthly” income is broken down for those employed only, such as base, OT, Bonus, Commission, or Military income and or other. Also note-able is the “statement” box dead smack in the middle of this area. If they are employed by some party involved in the transaction it must be identified.

The next section “if applicable” is for additional income. Meaning someone whom has two jobs for example. This is the section for that. ↓

Next up is the PREVIOUS employment section, again “if applicable” and current employment is less than 2 years. Note-able in this section is the fact on previous employment the client must provide previous monthly gross and identify if self employed. Known as section 1d.

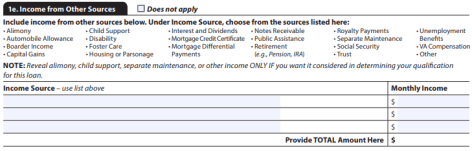

In the last section on page two, and rounding off section 1 of the new 1003 is section 1e. This identifies all “other” income. And the way it’s portrayed is a great reminder for LO’s to see as it lists all the other income types to remind you to ask.

Proceeding that at the way bottom left there is a line on page 2 at the bottom that identifies which client’s 1003 work information you would be looking at. I can see this one of those lines that drives LO’s nuts and is constantly left blank. This is why each person has a separate 1003 now. So even if they are married, just as section says at the top, you are identifying if that application is a “joint” or individually. And if with other’s you list the total number and names of all other’s that would have a separate 1003 associated with the transaction. Here’s a snip of the bottom of page 2. Get to know it is my opinion. 🙂

As always – #GetOnPoint with your own craft and know the 1003 like the back of your hand.