#MondaysMotivation – The new CFBP rule is out! And the black hole has been filled! The “old” 4 day rule is out, and the CFBP does a great job in giving clarity on what can “reset tolerances” in a loan. I think they got this one right for sure. It’s great to see regulators not only making the laws to help protect consumers, but revising the laws to provide clarity and ease of use!

Half the battle of all lending laws is having interpretation and implementation to systems and processes to help enforce them. In this round, the CFBP got it right. Check out the full video as I explain my interpretation, and how they make it easier to allow for a REVISED CD to reset tolerances.

As always I suggest you be more accurate than ever before upfront. In fact you should input fees’ less common and be prepared for “inspections” and other transfer fee’s upfront. No matter what it’s always better to go down than to go up.

This week I’m expanding my lending roster, and welcome helping your arsenal of lenders too! #LetsDoBusiness

#ThursdaysThoughts – Broker Compensation de-mythed! Debugged! What ever you want to say, I’m not a lawyer, but I am a great AE (Lender Rep). And I know what’s my opinion of a right compensation plan a Broker should have in place. This all came about in a thread on social media where one Broker asked if they could have multiple comp plans with different lenders. The real true answer is —- It depends on how you pay the Loan Originators and how your shop is set up.

I talk about every aspect the comp law rule does and break it down. Can you pay someone 1099 or do you have to W2? Can you lower your compensation during a loan? Can a Broker owner have multiple comp plans with different lenders? These are all viable questions for the small business owners of Mortgage Business Brokerages. Some answers are vague, and some answers are crystal clear in reading the final compensation law from 2013. (updated version is uploaded into Sales Talk with Mortgage Pro’s file’s tab) WARNING – This video is exactly 30 minutes, and one of the longest I’ve published. But I think it’s a great interpretation of how comp law needs to be implemented for you Mortgage Brokers out there. If you have questions let me know.

There’s a definite difference between how a Broker with LO’s they sponsor and a “One man Band” Broker shop would need to make sure they have their comp plans set up. The NUMBER 1 thing to ALWAYS think about is the definition of a PROXY! – Does the compensation to a loan officer vary in an audit of a bunch of a loans, and can the LO directly or indirectly influence the factors to charge more or less on any one loan. If the answer is yes, then you should do something about the way you have your comp set up.

So in other words, if a LO sponsored at a Broker shop has the ability to choose a lender and get paid a different amount, and you as a Broker charge a per file basis for example, your comp plan is set up wrong. They indirectly are being paid different percentages with different Lenders. If you have different comp plans with different lenders, but an internal comp plan to pay the LO the same amount regardless of where the loan is sent, then you are in compliance. So it all has to do with how you actually “pay the LO”. You are included in that definition Brokers. So if you’re a one man band, you can’t have various comp plans to be paid various amounts, unless so carefully constructed to pay the LO, indifferently based on another factor. That unless part is left ambiguous. But in a real example, can you have LO’s that specialize in reverse loans and that’s all they do, and they are paid X, while the LO’s that do forwards are paid Y. Well that’s a way it does look like it would work.

Remember this is my interpretation, and I’m not a lawyer. Nor does this apply to any lender that has a “line of credit” and are funding in their name. More scrutiny would need to be taken into consideration, especially if you have a direct “ticket” to sell to Fannie, Freddie and Ginnie. As well as any specific “State” rules. This is just a helpful interpretation for the mortgage Broker community of the lending comp law. Do your own due diligence, and read it. I’ve read it a dozen times in a week, just for this segment. And I don’t think it’s off by much, if any. Please construct your compensation plans to pay LO’s (including yourself) the same across the board when in the “third party origination” (TPO) space. *Remember PROXY rule.

Section 1026.36(d)(1)(ii) states that the amount of credit extended is not deemed to be a transaction term or condition, provided that compensation received by or paid to a loan originator, directly or indirectly, is based on a fixed percentage of the amount of credit extended; the provision also states that such compensation may be subject to a minimum or maximum dollar amount. The rule also further clarifies the definition of a proxy to focus on whether: (1) The factor consistently varies with a transaction term over a significant number of transactions; and (2) the loan originator has the ability, directly or indirectly, to add, drop, or change the factor in originating the transaction.

Last but not least, how I would do it. If I was a Broker, I’d have a set of lenders and different comp plans for different specialties. That way I can be competitive in all products in my area. I would have a comp plan that would give incentive to LO’s to self generate a loan, and pay them more on those, versus leads I provide them. I would have a Senior level pay plan and would give a bonus incentive to my LO’s based on volume over a quarterly period. I would pay each LO a set percentage of the credit extended and that percentage would always be less than my compensation with any one lender in my roster. The spread is for the house, and how I would be able to give bonuses for volume. I would prohibit borrower paid loans to vary less than 2% of the said comp plan for that originator. So they can’t “lower their comp” by a significant amount, but enough to defray unforeseen circumstances that happen with loans to “do the right thing” for Clients. I personally would pay myself according to the set percentage comp plan as well. As to avoid being paid various amounts this way based on the lender’s comp plan.

If you would like further help in custom tailoring a comp plan that can fit for your organization, I am open to discussing these things with my Broker’s. As my goal is to help you grow your mortgage company, close loans with my team, and help you source new business with marketing campaigns. #LetsDoBusiness

#WhackedOutWednesday – Estimate of Fee’s need to be made in “Good faith”! Hence why it was called a GFE in the past. The new name is Loan Estimate, the concepts of the fee’s are the same. The rules of what can change, what can NOT change and what fee’s have a 10% tolerance have been updated, but the consensus is the same. Nothing changed in how you should be putting together your estimates. Know this stuff!

Below I will place the current chart that breaks down each section, however there are somethings worth noting. A notable mention is the transfer taxes, go high on purpose. You don’t need to over estimate 1000’s of dollars, but to add a few hundred just in case is ok. Another notable is the SSPL, or Settlement Service Providers List, and how these fee’s labeled with a companies name in the beginning work. Know how using a different company can be loop hole to fee variances. Know how to calculate per diem interest and how to set up an impound account. While certain things can change, there’s a best practice to be more accurate than ever before now.

Below is the current FEE chart, that breaks down the various “areas” on the LE as to what can change, what can NOT change and what has a 10% tolerance. Know this, and get good at making estimates. Yes, you want to under promise and over deliver, but “Fee’s” in general need to be more accurate in the act of Loan Origination than ever before. The CFPB doesn’t want you way over disclosing and then making it a habit to reduce fee’s later on. They want you to make an estimate “In Good Faith”

#TwoforTuesday – HOPA to the rescue! PMI or Private Mortgage Insurance is a good thing, and explaining to clients how it works, what it’s for, and how it can be cancelled afterwards is all apart of making yourself stand out!

This comes in good timing as rates are going up, and Home Possible and Home Ready programs are more attractive as a result. In my group Sales Talk with Mortgage Pro’s, a seasoned LO, asked for a price check across the board and asked over 4000 people what their price was for a 30 yr fixed, 80 LTV. As a result I priced my own and found these two programs a potential “angle” they could pitch. The crowd loved it, and then PMI came up. One has it and one doesn’t. Well there’s advantages and disadvantages to this, in fact PMI is tax deductable up to a certain income bracket still. (married 109k or single 54k). Today I go over the two ways PMI can be cancelled to help you LO’s be able to explain how it works as a viable option to your clients.

Two for Tuesday – Give your clients options, a Government option and a Conventional with PMI option. Look at saving them money in the bank and using the Home Ready or Home Possible options, then explain PMI to them. As a result (assuming they qualify) this can help you stand out as the professional.

#MondayMotivation – Get JUICY with Non-QM – Join Us In Creating Yes’s from investors that want an easy loan to expand their portfolio of homes this summer. An easy 10 day close, with Title, Appraisal and verified funds! There’s no debt ratio on this loan, yep, NO INCOME. And NO RESERVES needed, and you can close in a LLC, and can have 100+ homes financed. No problem. This loan is golden for investors doing it right and want to expand their list of investment homes or want to take cash out of one to do improvements.

Today I go over a few updates that are FRESH OFF THE PRESS, to this program as a whole. We updated the full matrix of guidelines for our Non-QM loan. Check it out below ↓

This week I am on the hunt for more Mortgage Broker’s that could use our products in their lender list! If you don’t have this NINR in your lender arsenal, let’s chat, I’m expanding to help as many as I can!

#WeekendCalltoAction – Create campaigns for a niche! This is how the most effective marketing campaigns get you results. Don’t just state your a jack of a trades and master of none, segment in your marketing. This is what will draw all types of loans.

All this week I went over #StrikeZones for me and #TeamNDM, while we have others, I focused on our strong suits and the loans that create the best campaigns on purpose. This weekend I suggest you do the same. Don’t just “pick a niche” and then find an audience. Do it backwards. Find the audience you want to market too, then market to them what can be a solution for them. That’s “niche” marketing at it’s finest.

I am in the office taking “I gotta guy” questions all day! – If you don’t have an Lender Rep that can help you close loans and source new business, let’s connect! Fill in below and I’ll call you next!

#ThursdaysThoughts – The best loan in the market hands down in my opinion. And a great strike zone for me. If you mortgage Broker’s send in a check for 100 dollars to any lender to sponsor you on VA loans we should be one of them!

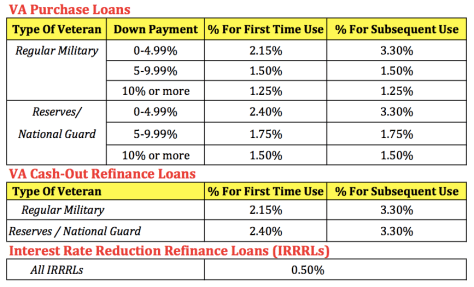

VA loans are great, but there are a few things that can “haunt” you if you do them wrong. 1st, make sure you ALWAYS disclose the highest funding fee upfront. Today I go over a few other tricks and tips and also provide the “Funding fee” chart below to help you and the VA residual test link to double check your calculations. Check it out below ↓

Below I will post the charts for VA funding and a residual income calculation to help you set up your VA loans for success!! 🙂

VA loans rock, and we price very well on these loans, #LetsDoBusiness!! I’m in the office all day taking “I gotta guy” questions to help others on guides!

#WhackedOutWednesday – The most under utilized program is the USDA loan in my opinion. And today, because it is a #StrikeZone for me, I wanted to highlight some things for you mortgage pro’s. This is a fantastic program, and guidelines and “zones” have been updated. You’ll be surprised, you might find this is a great loan to segment an advertising campaign with.

I’m including a few links today, and the 1st will be a link to gain GUS approval on your end. Many Broker’s seem to not have this set up, and you can do so right from my website. 2nd link will be the calculator to help you see if someone qualifies for this loan. I go over several guidelines you should know, from what constitutes a large deposit to DTI ratios to look for.

I believe this is a great program, and a #StrikeZone for me. Here’s the links to help you;

The link for the GUS sign up for you brokers — CLICK HERE!

The link for the qualification calculator for USDA —- CLICK HERE!

For those of you that like ideas to source new business, here’s definitely one of them to segment and see if there’s a USDA zone near you. #SellWell

#TwoforTuesday – Cheaters never win! Fannie Mae’s newest update stops them. Funny but this is the truth. Why are we in 2018 and we still are dealing with “Cheaters” in the mortgage industry. There are some great companies out there and it’s appalling to hear these stories where companies are doing things to cheat and use lender credits for a down payment. Are you kidding me, you played some loop hole for years just cause? It’s the same for builders that are giving excessive incentives to a borrower to capture both the Real Estate side and Mortgage side of the equation. Then taking it away or not offering it if another lender is used. I am not so sure about the whole KW thing going down right now. I don’t have an opinion yet, but if they are blatantly “cheating” to incentivize, this is the ethical stuff we need to ban from our industry.

Fannie Mae issues two new changes at the beginning of the month due to those that needed clarity. Seems the first change is well, I understood it this way for years. Maybe I just didn’t look to cheat and use it that way. Crazy some people do this, and Fannie has to update verbiage and completely spell it out. Second change makes sense and is a helpful one to help those doing construction loans to define the transaction type. Check it out below ↓

What I feel like doing this summer is creating a list of builders (or other companies) that “cheat” and publicly posting it for those to see. This can’t go on, if you “cheat” and know it because you’re on the “other side” of some aspect of Real Estate, Title or otherwise and incentivize clients to use your company in a manner that’s abusive. You should be reported. Cheaters never win! Well some say maybe in the short term, but in the long haul there will be a cause and affect that might not be in your favor. Please please please execute good judgement and fair lending practices when in mortgages. It’s what makes it “right” for the client. “Do the Right thing” has always been apart of my mantra and it seems more and more companies are actually looking to play loop holes in our industry to gain a competitive edge. At least for a short lived time. If you know of a company doing something like this, let me know, I’ll show you the way to report them.

STOP CHEATING! – Fannie Mae shouldn’t have to put out guidelines to clarify a guideline that was set many years ago. (A lender credit was never intended to be used for a down payment or for compensating third parties) Nor should companies be incentivizing clients to use their services or steer them to use and not offer the same incentive if a borrower chooses another (Shop-able) option. Watch mark my word, down the road there will be legislation in our industry that if some incentive is offered to use a shop-able service for a mortgage (that is also owned by same mortgage company) there will be a limit or restriction of the incentive. Or something to the affect that another option is used, a percentage of that incentive would need to be applied. Something will happen in this area. Be fair to your clients, your brand and your way of doing business. Nothing good comes out of cutting corners. PERIOD>.

#WeekendCalltoAction – This is the wrap up of #ProcessingWeek and hope you enjoyed the videos and blog this week on tips and tricks to close your loans in 10 days or less. Funny thing is I have one loan right now where the LO didn’t “read” the DU and sent in more than what was needed, and that might kill the loan. (we’ll see). I wish there was a magic sauce to help everyone increase their business, but the reality is – it takes work. You actually have to “do” something. Just like getting loans closed quickly you have to take certain steps along the way!

If you do these things, and communicate with your borrowers, there’s no reason why you are not obtaining multiple referrals along the process of a loan. Especially if you plant the right seeds, paint the pictures of the process and help the clients truly “understand” what’s in their best interest. At the closing table you should be getting your second or third referral. Or a list for that matter! 🙂

#WeekendCalltoAction – Call every client you have in process and ask for any warm referrals. If they say no, ask for them to send you an email of people that you can call without mentioning their name! – Any way you can, get a name to call!

Today, I will be in the office taking “I gotta guy” questions to help others close the loans they have. If you are scarce on loans, let’s connect, I have some JUICE that can help you generate more business. Call me in the office. 304-901-2798 is the office line.