I think you’re gonna like this!! #TwoforTuesday – Fun edition – I got creative in the last week and got a new video opener! I am sure it will help Pump you up, and get ready for the day! Join Us In Creating Excitement and get the JUICE’s flowing! You’re in sales right? – #JUICE

Two for Tuesday as I always have branded is two tips on guidelines or something mortgage related that you can take with you in the field. Today’s topic – VOE’s and Pay Check Stubs! Yep, both are needed to calculate the right income, and both work coherently together. Supporting each other! #CheckItOut ↓

For those needing to gain more leads so they have more paycheck stubs to check and VOE’s to order – I got your back! I’m doing a discount for those that want to take charge of their 2018 and learn to earn on Social Media! If you have a fan page and it doesn’t get you leads every week, I can show you how to change that with my BLUEPRINT! It’s not rocket science and definitely not hard. In fact, it’s fun to have a social media presence and YOU can be known as the expert in your area!

Reach out to me, I’m here to help you take #SocialSelling to the next level in 2018! Sign up for the BLUEPRINT today! – Disclaimer – You do have to actually do work! lol #SellWell

#WhackedOutWednesday – QM Fails – Really?! You have a 400,000 dollar loan the borrower can’t even obtain any rate on the ratesheet? Really?! Yep, this stuff happens if you have a comp plan accustomed to Government loans. If your comp plan is 2.75 and you’re doing a cashout conventional loan that is getting killed by LLPA’s (loan level pricing adjustments) then odds are you could be in this situation too. Even with a 680+ FICO, depending on how the break down goes.

I want to share something today, a best practice tip and a way to look at this stuff to help you Broker’s and LO’s in TPO to avoid this mess. If you’ve been in mortgages long enough more than likely you’ve had some QM fail happen.

**Compliance disclosure – JUST FYI – You’re NOT supposed to just be able to switch from Lender paid comp, to borrower paid comp just for the purpose of passing QM. It specifically states that in the rules/laws. (I can show you if needed) Your Change of Circumstance must be recorded as something else. FYI

Ok now that’s out of the way, let’s look at a RATE SHEET! If you see the top of the rate sheet at the top rate pays back “less” than the rate below it, then the rate that pays back the most is the rate considered the “top”. Second, the SPREAD between the top rate and the next eighth below it will change pricing, but most likely “less” than a whole point. You have to go down probably two or three eighths’ in rate in order to have a whole point difference between the TOP rates premium. The KEY TO UNDERSTAND is that rate where the spread is more than 1 point (from the top rate) is where you can start to bonafide a discount point.

The simple way to look at this is to take the indifference after the bonafide discount point and add that to your comp plan. So if the rate picked was a COST of 1.125 for example… Your comp is 2.75, and as long as the (base premium before adjustments) spread between the top rate and the rate your picking is more than a point, you can bonafide a discount. So for example, 2.75 + .125 = LESS THAN 3. Assuming you have bought out the underwriting fee and there are no affiliate fees in the equation, this would pass QM.

Remember in order to bonafide a discount point you can NOT be at the top or the bottom of the rate sheet. (meaning highest or lowest rate) Sometimes I don’t even see how this is good for a borrower, but the reality is it is tied to the comp plan. If you are in the situation where the comp you have with that lender is higher, then watch or do a QM test PRIOR to submitting so you know what your up against. BEST ADVICE I CAN GIVE. Do not wait until the loan is submitted or even attempt to lock in process without having an idea of how this plays out. IN FACT, MOST LENDERS have a FREE QM test available on their “portals” that you can run this test as you register the loan. I suggest you know how to do this. Problem avoided. If you have questions about this hit me up, I’d love to help you understand how this works. In some cases it is #WhackedOUT – But hey these are the rules we have to play by. Lower your comp if you’re doing conventional loans, they don’t have a spread like the Govie loans do.

Another “argument” is this is why you have the ability to set up multiple different comp plans with different lenders. NO, in my opinion you do NOT need to have the same comp across the board with all lenders. The law doesn’t say that. (for Broker’s of course). What it does say is that each LO (MLO) should be paid the same based on type of loan. And be incentivized based on volume. But that is another post for another day. – #SellWell

#TwoforTuesday – Non-Traditional groups are needed to help when someone needs to qualify with non-traditional credit. There are two groups that you need three things from. I will detail this today in efforts to help you pre-qual someone whom has “thin” credit. NEED ALTERNATIVE TRADE LINES? Here’s what you need to know;

There are two groups, and you need at least 1 thing from group number 1. Group 1 consists of Rental history, a utility company, or telephone service. Group 2 can consist of a personal loan, insurance payments (car, medical, renters, life), Child care payments, rent to own payments, or school tuition. This second group also consists of car lease (rental) payments or retail store credit cards, however I don’t know why an auto lease or retail store wouldn’t report that to the bureaus though. lol

Here’s a break down of guides for you: Happy Selling!

I am helping LO’s left and right learn how to generate business online. No doubt anyone can do this and dominate in their market. My suggestion, get going start social selling today! It changes people’s whole outlook on how they use social selling when they start seeing results. (Facebook is no longer just for Friends and Family)

Get involved implementing the BLUEPRINT today, it will change your pipeline 30-60 days down the road. Don’t struggle into the new year, get growing today! Learn how to set up your business fan page to actually get you leads. Learn the best posts to drive engagement and interaction. And learn how to set yourself up to gain more referral partners! – This is only 250 dollars – If you are an action taker, I would ♥ to work with you! You will double your business by implementing the BLUEPRINT.

#TwoforTuesday – A trick to remembering how long someone needs to have been receiving income to use it on a FHA loan. And a tip to add value right now and gain more purchase business. Short and sweet today. I got leads to call. Do you?

NEED LEADS? Is it COLD there? No weather pun intended. What I’ve done over the past two years is lead by example in creating organic presence on various social media platforms. If you do not know or “like” and “follow” my fan page on Facebook, please do! Click HERE to See my FAN PAGE! Technically it’s a hub of resources within it that any Broker or Mortgage LO can use to help #SellThemselves and gain leads for FREE>

In fact, I have a whole program that I do just this with Broker’s and individual LO’s that want to step up their #SOCIALSELLINGGAME!! I teach how to plan campaigns weekly on social media business pages to allow those that want to take advantage of social media’s reach. I teach how to set up a page, to how to push and pull your messages into social media land and gain leads FREE on a weekly basis.

Want to gain #theBLUEPRINT to doing so yourself? Click BELOW ↓

#MondaysMotivation – Guides for LO’s all week this week. We will start with a simple cheat sheet for DTI on FHA loans. A great thing to know, and guide to basically live by. Too many times I see LO’s wasting time attempting to put a file together that is way out of the ball park. And DU confirms my thoughts and then they ask me to do a manual, I tell them the same “chart” I go over in today’s video and tell them to restructure.

Use this as a guide;

#SellWell – If you are a mortgage Broker and you’re not hooked up with me, let’s work together in 2018!

#TwoforTuesday – Application guidelines today! And a cheat sheet for FHA UFMIP refunds! Got to ♥ it! Lender paid and Borrower paid I will be posting more of and how you Broker’s can WIN every deal no matter what any direct lender gives the client.

As a mortgage Broker owner, you should know how to go both ways, Borrower paid or Lender paid. If done correctly, you can effectively meet and beat any offer any “bank” gives your client. Rates are Rates, and more and more clients realize that there are combinations of rates and fees that go into loans. (well more LO’s are teaching this now more than ever before – Great work)

When a client asks for ARM pricing (Adjustable Rate Mortgage) you as an LO, must show certain things to them upon “Interest” and or applying for an ARM loan. Great Application guidelines to know! #Checkitout ↓

#TGIF – The Grind Includes Friday (everyday for me) 🙂 – Very frequently I am asked about rules of the 1003, and wanted to drop two commonly asked questions as guides today. Number 1, the 1003 is going to changed, yep you’re going to have to learn a new one! But not until 2019. So you still have 1 more year with the current version of the URLA. So good news there. Number 2, the most commonly asked question I get asked is about the work history. Most get confused about the rules for using income, and how to fill out the 1003. Let me clarify. – You need to detail a 2 year housing and a 2 year work history on the 1003. It’s as simple as that. If they have only worked at their current job for 30 days, just keep asking the client “where did you work prior to that?”. Make sure you detail 2 years as a history of working. Now high school does NOT count, but trade schools and college do. If there is more than 30 day job gap all you need to do is get a letter of explanation from the client (loe/lox). Simple. Number 3, the rule of 5. I love this rule. And many do not know it. So here’s a cheat sheet to refer too. Commission, bonus, over-time, self-employed or working two jobs are the 5 things in this rule. And really you only need a TWO YEAR HISTORY OF WORKING TWO JOBS AT THE SAME TIME! The rest of the rule of 5 you only need a 1 year history of doing. With exception of being self employed and actually working in the same field for 2 years or more, but you can be self employed for 1 year only and do a home loan.

Better yet, you can use our #SponsoroftheWeek PERFECT LO to help you take an accurate 1003 from the start! #SellWell

I’m growing again and today calling Broker’s I do NOT know at all. If you watch this, share it with a fellow Broker or Bank that could use a great Account Executive to help them close more loans and gain more business! #FilloutBelow

#WhackedOutWednesday – Today’s installment is all about collection accounts for FHA and Conventional guidelines. There’s some JUICE in here that you may not know. #Checkitout PS>>> I’m accepting transferred appraisals and new FHA submissions 🙂

Check out the #SponsoroftheWeek whom is; CARD TAPP APP

A virtual business card can help you “track when to strike”! #SellWell

I ♥ GOVIE LOANS, USDA, VA or FHA are a specialty of mine. I do these loans for my Broker #partners down to 560 FICO! Today being #TwoforTuesday I wanted to address the up front insurance fees and monthly MI’s for all these programs. And provide a guide on this that could help you remember them.

#CardTappApp is the Sponsor this week and can custom tailor any app for the sales your in. The owner was a #MortgagePro that was seeking to gain more exposure! #Checkitout CARD TAPP APP – CLICK HERE

I WAS WRONG! LOL, I remember that majority of FHA loans are typically over 90% LTV and not a 15 year. But I am placing the charts for each product below;

FHA FIRST:

Here’s where I was wrong, looks like if you have less than 78% LTV on a 15 year FHA loan the MI stays on the loan for 11 years and can fall off. I guess I forgot that 🙂

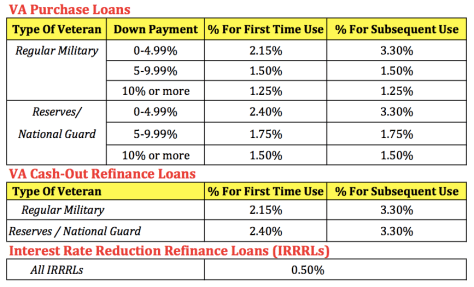

NEXT IS VA, I ♥ VA loans and it seems my Brokers educate me on this loan more than any. The guidelines are so awesome for this loan, did you know you can payoff debt with sellers contributions? Check out the Chart below and identifies based on the “branch of military” what the funding fee is;

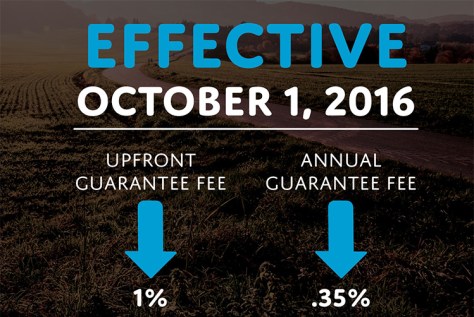

And Last but certainly not least the chart for the USDA Guarantee fee;

#PrayerstoVegas – Wore the hat out of respect, what an unfortunate event. This week I go into guidelines to add value for all. I am partnering with new Brokers, and Banks in October, sign up below; This weeks new sponsor is CARD TAPP APP – A virtual business card that tracks when your clients look at it. You get notified, and there are even ways to co-brand with others. Great sales tool! CARD TAP APP WEBSITE

Talking FHA or VA? Price me out today, PM me, send me an email, reach out on LinkedIn or Facebook, I’d love to show you our rates. #Letsworktogether